FUTURE SERVICING OPPORTUNITIES

Each year, around 1.1 million vehicles reach five years of age, a key inflection point when it comes to where they get serviced and maintained

Regardless of whether this is due to them exiting their new vehicle warranty, the finance being paid off, reaching the end of pre-paid or capped price servicing, becoming more expensive to maintain, or just changing hands, these triggers can all prompt a shift away from dealership workshops and into the aftermarket.

This is supported by data from the Fifth Quadrant Consumer Tracker1, with 75 percent of used car owners servicing in the aftermarket, compared to only 52 percent of new car owners.

For independent workshops and aftermarket suppliers, this therefore marks a crucial point for customer acquisition and long-term business opportunities.

Understanding the upcoming shifts can help operators make better choices when it comes to business planning, staff training, equipment investment and customer relationship building.

Planning for a changing vehicle landscape

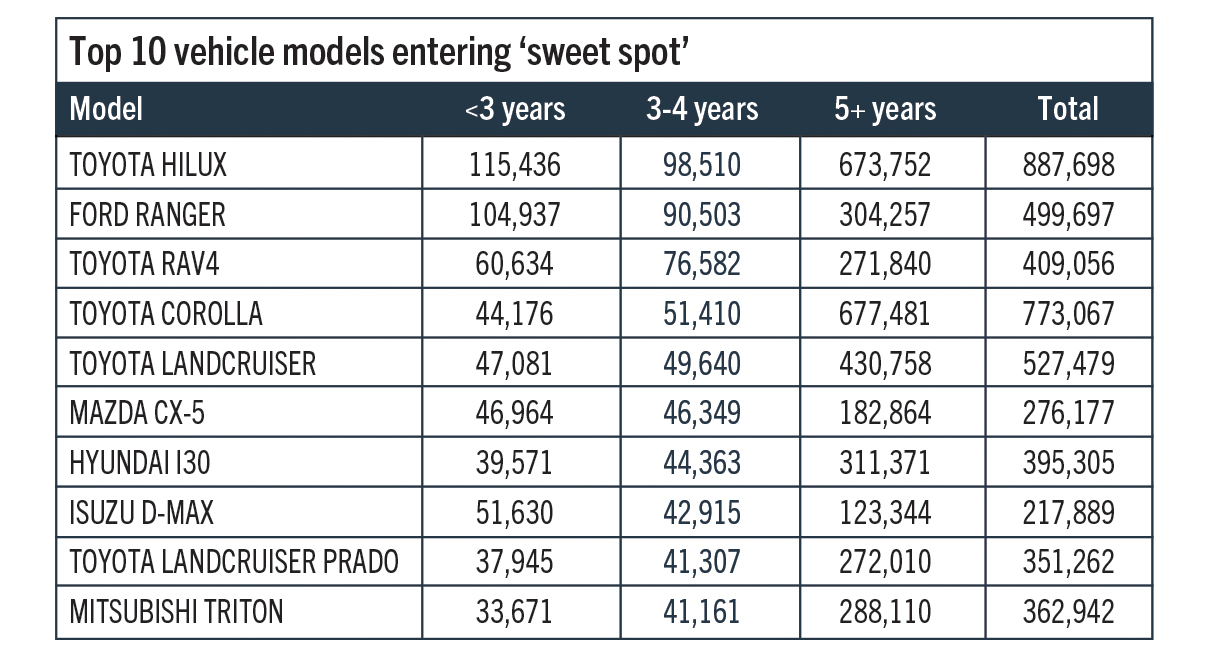

Looking at the three to four-year-old vehicle cohort in BITRE car parc data2, we can see that the top 10 models make up around a quarter of the vehicles that will tick over this milestone within the next 24 months.

The reality though is that we need to start with the top three, given they account for more than a quarter of a million vehicles.

There’s no question that workshops should be set up to service Toyota’s top-selling Hilux and RAV4 models, as well as the Ford Ranger, but they will clearly need to maintain this expertise well into the future.

Looking further down the list though, we can see some newer entrants, with models like the Isuzu D-MAX likely to grow its ‘addressable market’ by around a third over the next two years.

The link to the used vehicle market

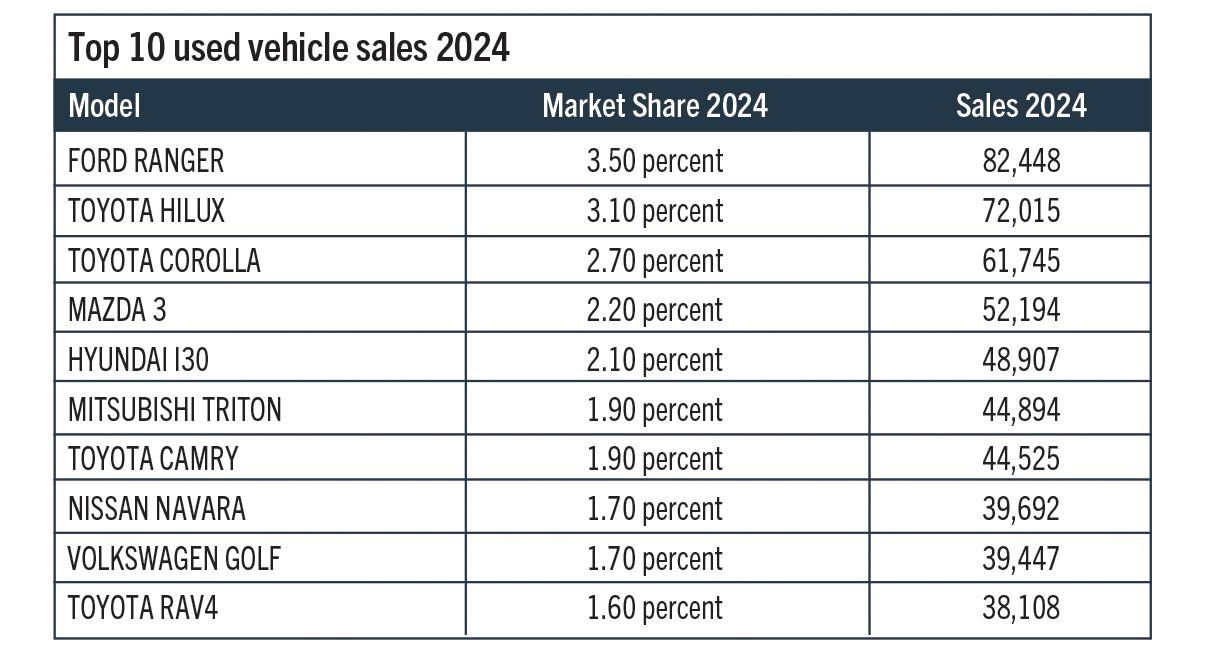

Second-hand vehicle sales are another strong indicator of aftermarket servicing demand, given second or subsequent purchasers don’t have the same emotional connection to the dealership.

According to the 2024 Australian Automotive Insights Report3, many of the top-selling used vehicles are the same as on our previous list, but there are some important differences:

- The Toyota RAV4 goes from third on the previous list to tenth here, suggesting owners might be holding these longer, and delaying their entry into the aftermarket

- The LandCruiser and Prado both drop off this list, suggesting that they are also being seen as longer-term ownership models (but likely more among 4WD enthusiasts)

- The Corolla moves up to third on this list, while three of the four models that weren’t on the first list are also smaller passenger cars (Mazda 3, Toyota Camry, and VW Golf), talking to the longevity and lasting popularity of these models.

Key Takeaway

As vehicles exit warranties, change hands, or become more costly to maintain, the aftermarket must adapt to a changing car parc.

With that said, many of the vehicles entering the aftermarket in the near future are likely to be ones that workshops are already well prepared to service and maintain.

The question marks are more about the longer-term horizon, given the unknown impact of NVES on sales of utes and larger SUVs, the new brands entering the market, and the ongoing shift to electrification.

In fact, for the aftermarket, the next few years might well be the ‘easy’ bit.

This column was prepared for AAA Magazine by Fifth Quadrant, the AAAA’s partner in the Quarterly Aftermarket Dashboard Summary Report which is delivered to members each quarter, and the Interactive Digital Aftermarket Dashboard (available in the member area of the AAAA website).

For more information about their services, visit www.fifthquadrant.com.au or contact Ben Selwyn at ben@fifthquadrant.com.au

- Fifth Quadrant Consumer Tracker, March, April and September 2024.

- The Bureau of Infrastructure and Transport Research Economics (BITRE): 2024 Release

- AADA x AutoGrab Australian Automotive Insights Report 2024